The word mediclaim is one of the most misused terms in Indian insurance. Millions of people say they “have a mediclaim” when they mean any health insurance policy. Understanding what a mediclaim policy actually is — and how it technically differs from modern comprehensive health insurance — matters when you need to make a claim and discover your coverage is narrower than you assumed.

What is a Mediclaim Policy?

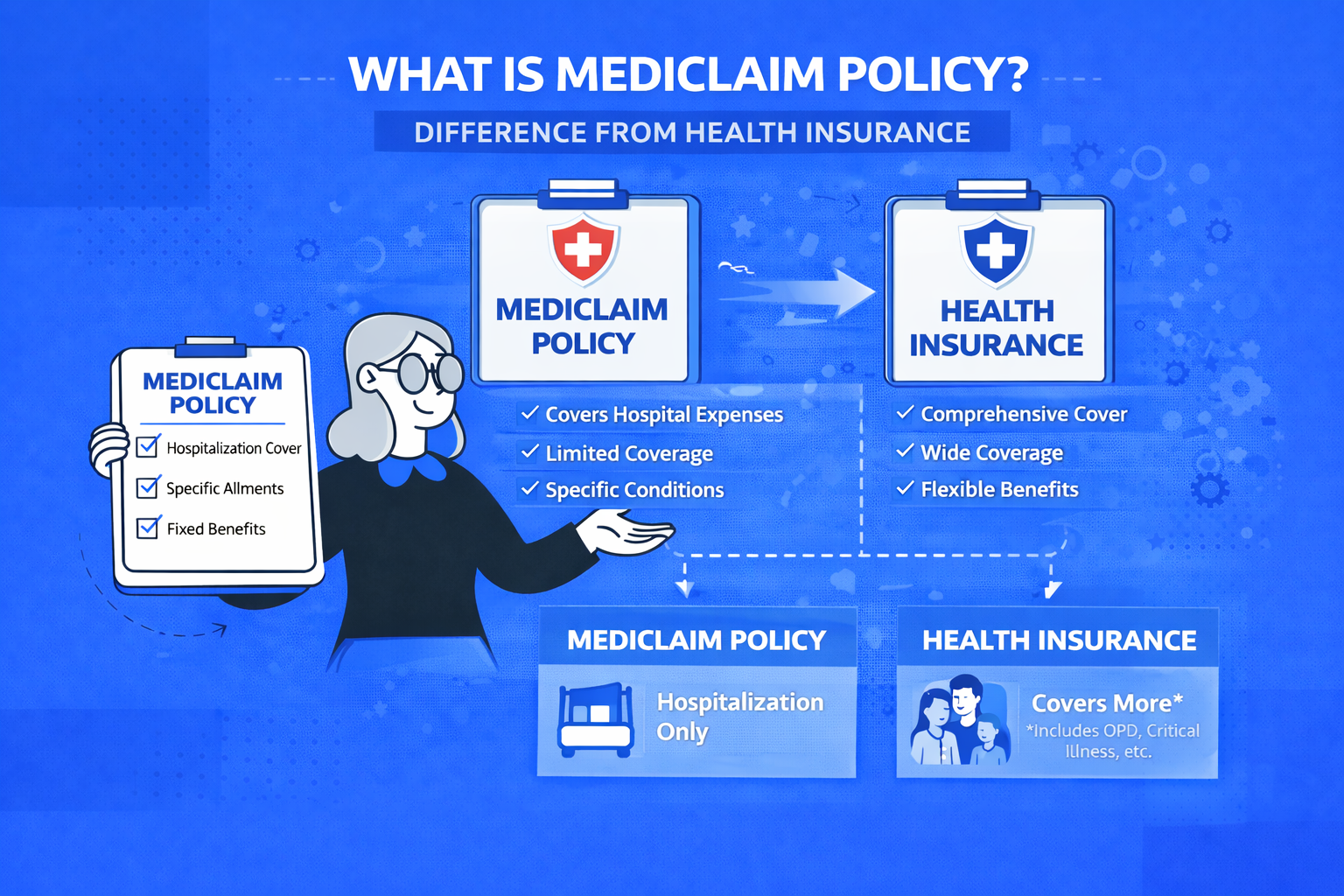

A mediclaim policy is a basic hospitalisation indemnity insurance product. It reimburses (or cashlessly pays) the actual medical expenses incurred during a hospitalisation of at least 24 consecutive hours.

The key word is hospitalisation. A classic mediclaim policy covers:

- Room rent — the daily room charge during the hospital stay

- Doctor and surgeon fees — consultation, surgery, anaesthesia

- Nursing charges — nurses assigned during the stay

- ICU charges — intensive care unit costs if required

- Medicines and consumables — drugs and materials used during the stay

- Lab tests and diagnostics — tests conducted while admitted

- Ambulance charges — typically limited to a fixed amount

What a basic mediclaim policy does not include:

- Outpatient (OPD) consultations

- Pre-hospitalisation expenses before admission

- Post-hospitalisation expenses after discharge

- Day care procedures (unless specifically added)

- Maternity expenses

- Dental or vision treatment

- Critical illness lump sum payments

The Origin of the Word “Mediclaim”

The term comes from United India Insurance Company, which launched one of India’s first hospital expense policies under the brand name “Mediclaim” in the 1980s. The policy became so popular that the word entered common usage for all hospitalisation insurance — similar to how “Xerox” became synonymous with photocopying.

Today, IRDAI and insurers use the term “health insurance” officially, but “mediclaim” persists in everyday usage, creating widespread confusion.

Mediclaim vs Health Insurance: Key Differences

| Feature | Mediclaim (Basic) | Comprehensive Health Insurance |

|---|---|---|

| Coverage scope | Hospitalisation only | Hospitalisation + pre/post + day care + OPD + more |

| Pre-hospitalisation | Limited (15–30 days in some plans) | 30–60 days in most plans |

| Post-hospitalisation | Limited (30–60 days in some plans) | 60–90 days in most plans |

| Day care procedures | Not covered or limited list | 500+ procedures covered |

| Domiciliary treatment | Rarely included | Included in many plans |

| Maternity cover | Excluded (unless a rider) | Available as add-on or in-built |

| AYUSH treatment | Usually excluded | Included in modern plans |

| Critical illness | Excluded | Available as a separate rider or plan type |

| OPD expenses | Excluded | Available as an add-on in premium plans |

| Sum insured options | ₹1–5 lakh (older plans) | ₹5 lakh to unlimited |

| Restoration benefit | Absent | Present in most modern plans |

| Premium range | Lower | Higher (but significantly more value) |

Why the Distinction Matters in a Claim

When you file a hospitalisation claim, both a mediclaim policy and a comprehensive health plan will pay room rent, surgeon fees, and lab tests during the admission.

The difference shows up at the edges:

Scenario 1 — Knee replacement surgery:

- Pre-admission physiotherapy consults and MRI: ₹18,000

- Surgery + 4-day hospital stay: ₹4,80,000

- Post-discharge physiotherapy (6 weeks): ₹22,000

A mediclaim policy pays only the ₹4,80,000 hospitalisation. A comprehensive health plan with 60/90-day pre/post coverage pays ₹5,20,000.

Scenario 2 — Day care cataract surgery:

- Procedure completed in 4 hours (no overnight stay): ₹55,000

A mediclaim policy may not cover this (below the 24-hour minimum). A comprehensive plan with day care cover pays in full.

Scenario 3 — Follow-up visits after discharge:

- Medicines, dressings, follow-up consultations for 45 days: ₹8,000

A mediclaim policy: not covered. A comprehensive plan: covered under post-hospitalisation benefit.

The 24-Hour Hospitalisation Rule

Traditional mediclaim policies require a minimum 24-hour inpatient stay for a claim to be valid. This rule was introduced when most treatments genuinely required overnight admission.

Modern medicine has made many common procedures — cataract surgeries, knee arthroscopy, kidney stone removal, chemotherapy sessions, angioplasty in some cases — day care procedures completed in hours. Comprehensive health insurance plans explicitly list hundreds of day care procedures that are covered despite being under 24 hours.

If you are holding an older basic mediclaim policy, check whether it has been updated to include day care procedures, or whether you are at risk of having common procedures rejected.

Group Mediclaim Policies: What Your Employer Actually Gives You

Most employer-provided health cover is technically a group mediclaim policy — a basic hospitalisation product negotiated at a group level. These typically provide:

- ₹2–5 lakh sum insured per employee (sometimes including family)

- Basic hospitalisation cover

- Limited or no day care coverage

- No portability (lapses when you leave the job)

- No personal waiting period continuity

Limitations to know:

- The sum insured is often insufficient — a single cardiac event, cancer round, or multi-week ICU stay can easily exceed ₹5–10 lakh

- Coverage stops the moment you change jobs or are laid off

- Family coverage may have a combined sub-limit

- Pre-existing conditions may be covered under the group plan but will re-trigger waiting periods if you try to port to an individual plan later

This is why financial advisors consistently recommend holding an individual comprehensive health insurance plan alongside any employer group mediclaim.

When a Basic Mediclaim Policy Is Sufficient

A basic mediclaim policy may be adequate if:

- You are in your 20s, healthy, with no family medical history of concern

- You already have a comprehensive employer plan and want only secondary coverage

- You are supplementing with a large super top-up plan (₹1 crore cover with ₹10 lakh deductible) at minimal premium

- You are on an extremely tight budget and need any hospitalisation safety net over nothing

In any other scenario — especially if you have dependents, are above 35, or have any pre-existing conditions — a comprehensive health insurance plan is clearly the better choice.

Modern Plans Have Blurred the Line

IRDAI’s 2020 standardisation and subsequent guidelines have moved the industry toward more comprehensive products. Most plans sold today are substantially more than the original mediclaim concept, including:

- Unlimited restoration of sum insured

- No room rent sub-limits

- Unlimited day care procedures

- Mental health coverage

- Pre-existing disease coverage with shortened waiting periods

- OPD coverage as an add-on

Technically, calling these products “mediclaim” is incorrect — but the word persists in popular usage.

The Right Way to Think About It in 2026

Instead of asking “should I get mediclaim or health insurance?”, the better question is: “Does my current policy cover the scenarios most likely to create a large, unexpected expense?”

Run through this checklist:

- Does it cover day care procedures?

- Does it cover 60 days of pre-hospitalisation and 90 days of post-hospitalisation?

- Does it have an adequate sum insured (₹15 lakh minimum for a metro adult in 2026)?

- Does it restore sum insured after a major claim?

- Does it NOT have co-payment clauses that force you to pay 10–20% of large bills?

- Is it portable — does it stay with you regardless of employment?

If any of these are “no”, you have a basic mediclaim policy, not a comprehensive health plan — and you should consider upgrading.