When you are admitted to a hospital and present your health insurance card for cashless treatment, the hospital does not call your insurance company directly — in many cases, it calls a TPA. Understanding what a TPA is, what it does, and how its involvement affects your claim experience is essential knowledge for every health insurance policyholder.

What Does TPA Stand For?

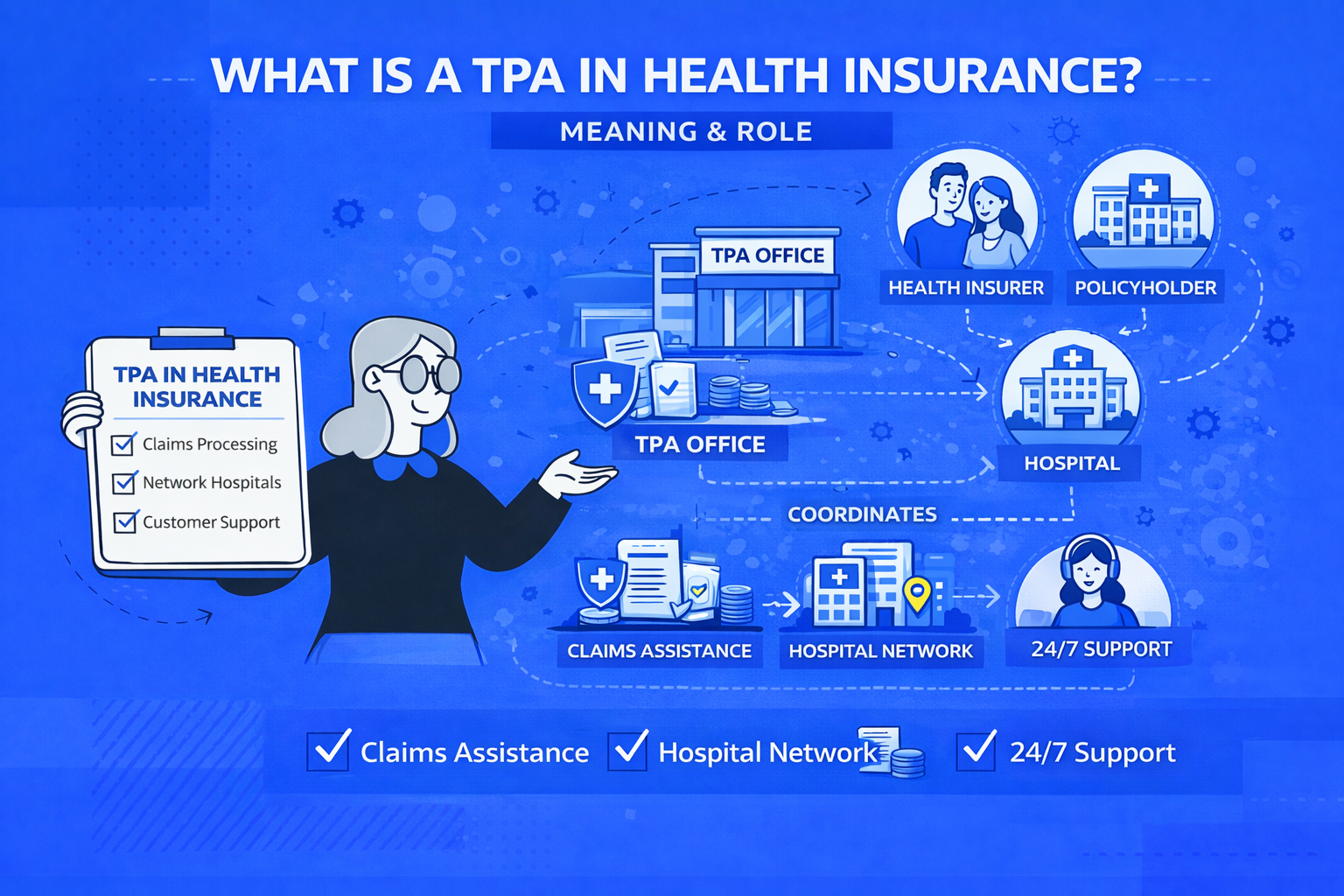

TPA = Third Party Administrator

The “three parties” are:

- You — the policyholder

- The insurer — who underwrote the policy

- The TPA — the third party who administers the health claim process on behalf of the insurer

TPAs are licensed by the Insurance Regulatory and Development Authority of India (IRDAI) under the Insurance Regulatory and Development Authority (Third Party Administrators – Health Services) Regulations, 2016. They are not insurers — they cannot underwrite policies. They are operational service providers.

What Does a TPA Actually Do?

A TPA handles the administrative and operational workload of health insurance claims so the insurer can focus on underwriting and financial management. Specifically:

During Cashless Hospitalisation

- Eligibility verification — Confirms your policy is active, the admission date falls within the policy period, and the treatment is covered

- Pre-authorisation — Formally authorises the hospital to begin treatment under cashless arrangement, specifying the approved amount

- Query handling — Requests additional medical records or documents from the hospital if needed

- Incremental authorisation — If treatment extends beyond what was initially authorised (e.g., complications arise), the TPA processes additional authorisation

- Discharge clearance — Coordinates with the hospital billing team and insurer to process the final bill before you are discharged

During Reimbursement Claims

- Document review — Receives and checks hospital discharge summaries, bills, prescriptions, lab reports

- Claim scrutiny — Checks that the claim falls within policy terms and conditions

- Recommendation to insurer — Sends a claim processing recommendation to the insurance company

- Claim settlement coordination — Once insurer approves, coordinates payment transfer

Network Hospital Management

- Maintains and updates the list of network hospitals empanelled under each insurer

- Manages the hospital empanelment process

- Handles hospital rate negotiations

Health Card Issuance

- Issues TPA health cards bearing your policy details, which hospitals use to verify your coverage

Major TPAs Operating in India (2026)

| TPA | Insurers Served |

|---|---|

| Medi Assist | Star Health, multiple PSU insurers, group policies |

| Vidal Health (formerly GENINS) | Multiple private and PSU insurers |

| Health India TPA | New India Assurance, Oriental Insurance, group policies |

| Paramount Health Services | United India, National Insurance, various group covers |

| MDIndia | National Insurance, Oriental Insurance |

| Raksha Health Insurance TPA | Various group and retail policies |

| Safeway Insurance TPA | Various insurers |

In-House Claims Processing: The Alternative to TPAs

A significant shift in the industry is that many leading private insurers have moved to in-house claims processing — eliminating the TPA and handling claims directly through their own internal teams.

| Insurer | Claims Model |

|---|---|

| HDFC Ergo | In-house (dedicated health claims team) |

| Niva Bupa | In-house |

| Care Health | In-house |

| ICICI Lombard | In-house |

| Star Health | In-house for most claims |

| ACKO | In-house (fully digital) |

| Bajaj Allianz | In-house (most policies) |

| Tata AIG | In-house |

| PSU insurers (New India, National, United India, Oriental) | TPA-dependent for most retail policies |

Why Does In-House vs TPA Matter?

In-house processing advantages:

- Single point of contact (insurer’s own team) → faster resolution

- No communication delays between TPA and insurer

- Better claim context because underwriting and claims data is in one system

- Escalation path is cleaner

TPA disadvantages:

- Potential delays in TPA ↔ insurer communication

- TPA staff may have less authority to make exceptions or contextual decisions

- Hospital staff sometimes unfamiliar with which entity to contact for a specific query

- TPA may use different hospital rate schedules than insurer expects

When comparing plans, in-house claims processing is a quality indicator — all else equal, prefer it.

How to Use Your TPA Health Card

When admitted to a network hospital:

- Present the TPA health card at the insurance/billing desk at admission

- The hospital will call the TPA helpline (printed on your card)

- TPA verifies your policy is active and the treatment is eligible

- TPA issues a pre-authorisation number to the hospital

- Treatment proceeds; all eligible bills are settled directly between hospital and TPA/insurer

- At discharge, review the final bill — confirm that all insured items are being processed and your out-of-pocket amount is only for explicitly excluded items (consumables, if not covered; co-payment, if applicable)

Important: Keep the pre-authorisation reference number. If there are claim disputes later, this is the primary reference document.

Common TPA-Related Claim Problems and How to Handle Them

Problem 1: TPA rejects pre-authorisation citing “not covered”

- First step: Ask the TPA to specify the exact policy clause under which they are declining

- Second step: Review your policy wording against the cited clause

- Third step: If you believe it is incorrectly declined, call the insurer’s customer service and cite the TPA pre-auth reference number — they can override TPA decisions

Problem 2: TPA delays are holding up discharge

- This is unfortunately common, especially in PSU insurer + TPA setups

- Call the TPA helpline, cite your pre-auth number, and escalate to the insurer directly if hold time exceeds 2 hours

- For time-critical situations, you may pay and file for reimbursement to avoid medical delay

Problem 3: TPA health card has wrong information or hasn’t arrived

- Contact both the insurer and TPA immediately

- Most policies can be verified via policy number + date of birth even without the physical card

- Download the digital health card from the insurer’s app if available

Problem 4: Hospital says your insurer is not empanelled

- Ask for the TPA helpline number from the hospital and verify directly

- Network hospital lists are updated frequently; hospitals sometimes have outdated information

- If genuinely not in the network, file for reimbursement

IRDAI’s Role in Regulating TPAs

IRDAI licenses TPAs and sets mandatory service standards:

- Pre-authorisation response time: TPA must respond within 2 hours for planned admissions

- Emergency pre-authorisation: Immediate, without prior documentation

- Claim documentation to insurer: TPA must transfer received documents within prescribed timelines

- TPA grievance portal: Policyholders can escalate TPA-related grievances via IRDAI’s Bima Bharosa portal (bimabharosa.irdai.gov.in) or the Insurance Ombudsman

If a TPA is non-responsive or wrongly denying claims, IRDAI complaints are a legitimate and effective escalation path.

Key Takeaway for Policyholders

Understanding TPAs matters most in these two moments:

-

When buying a policy: Ask whether claims are handled in-house or through a TPA. In-house is preferable. If TPA-based, find out which TPA and check their reputation.

-

During hospitalisation: Know your TPA’s helpline number (on your health card), keep your pre-authorisation reference number, and escalate to the insurer directly if the TPA process stalls.

For most retail policies from leading private insurers in 2026, TPA involvement is minimal or absent — your main interface is the insurer’s own claims team or a fully digital app. This has significantly improved the claim experience compared to five years ago.