Room rent sub-limits are the single most common source of claim disputes in Indian health insurance. A policyholder admitted to a hospital assumes their ₹10 lakh cover will pay for the hospitalisation — and is then surprised when the insurer settles ₹3.8 lakh out of a ₹6 lakh claim because of a ₹5,000/day room rent cap they overlooked at purchase.

This guide explains exactly how the mechanism works, with the arithmetic, the regulatory context, and how to evaluate plans against this clause.

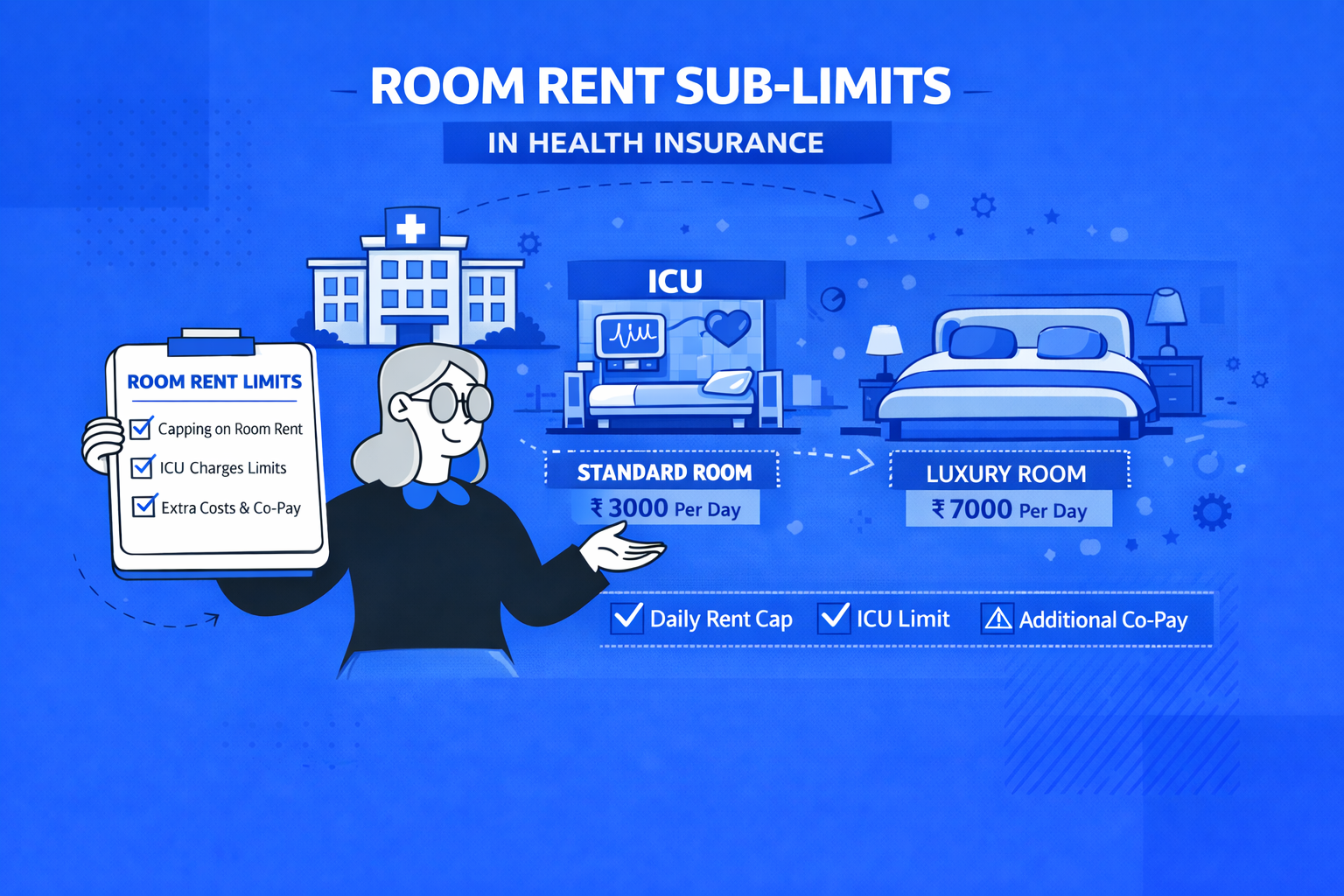

What a Room Rent Sub-Limit Is

A room rent sub-limit (also called a room rent cap or room rent clause) restricts the daily hospital room rate your policy will cover. It appears in the Schedule of Benefits — the table in the first few pages of your policy document that lists what is covered and at what level.

Two common formats:

Fixed rupee cap: “₹3,000 per day”, “₹5,000 per day”

Percentage of sum insured: “1% of sum insured per day” — for a ₹5 lakh policy, this means ₹5,000/day

The cap applies to the base room (private ward, single private room) and cascades to ICU limits, which are typically set at 1.5–2× the room rent cap.

What Counts as Room Rent

The room rent line on a hospital bill includes the bed, basic nursing, and accommodation. It does not include doctor visits, surgery, medicines, diagnostic tests, or ICU equipment — those are separate billing items. The sub-limit applies to the room rent line specifically; however, the proportionate deduction applies to everything else.

The Proportionate Deduction Mechanism

When you occupy a room that costs more than your policy’s room rent limit, the insurer does not merely deduct the excess room rent. It applies a proportionate reduction to all associated charges.

The Formula

Admissible Room Rent Ratio = Policy Room Rent Limit ÷ Actual Room Rent Charged

Payable Amount for Each Expense = Actual Expense × Admissible Room Rent RatioA Worked Example

Policy: ₹10 lakh sum insured, 1% SI room rent cap = ₹10,000/day

Actual hospitalisation:

- Room occupied: Single AC room at ₹18,000/day for 5 days

- Surgeon fee: ₹80,000

- Anaesthetist: ₹15,000

- ICU (2 days at ₹30,000/day): ₹60,000

- Medicines and consumables: ₹25,000

- Diagnostic tests: ₹20,000

- Total billed: ₹2,90,000

Admissible room rent ratio: ₹10,000 ÷ ₹18,000 = 55.6%

| Expense | Billed | Payable (×55.6%) |

|---|---|---|

| Room rent (5 days at ₹18,000) | ₹90,000 | ₹55,600 (excess ₹40,000 deducted) |

| Surgeon fee | ₹80,000 | ₹44,480 |

| Anaesthetist | ₹15,000 | ₹8,340 |

| ICU (2 days) | ₹60,000 | ₹33,360 |

| Medicines | ₹25,000 | ₹13,900 |

| Diagnostics | ₹20,000 | ₹11,120 |

| Total | ₹2,90,000 | ₹1,66,800 |

The policyholder pays ₹1,23,200 out of pocket — 42% of the claim — despite having ₹10 lakh of cover and a total claim of under ₹3 lakh.

Why Room Rent Sub-Limits Matter More in Metro Cities

Hospital room rates are not uniform across India. A single AC private room in a mid-tier corporate hospital in Mumbai or Delhi costs ₹12,000–₹20,000/day. The same room category in a Tier-2 city hospital costs ₹5,000–₹9,000/day.

| City Tier | Standard Private Room Rate | 1% SI Cap (₹10 lakh policy) | Gap |

|---|---|---|---|

| Mumbai / Delhi / Bengaluru | ₹15,000–₹20,000/day | ₹10,000/day | ₹5,000–₹10,000/day excess |

| Pune / Hyderabad / Chennai | ₹7,000–₹12,000/day | ₹10,000/day | Marginal or none |

| Tier-3 cities | ₹3,000–₹6,000/day | ₹10,000/day | No gap |

A ₹10 lakh policy with 1% SI cap may be effectively uncapped for a buyer in a Tier-3 city, while causing significant proportionate deductions for a metro buyer at the same hospital.

IRDAI’s Position on Room Rent Sub-Limits

IRDAI’s Master Circular on Health Insurance (2024) does not prohibit room rent sub-limits — they remain a permitted policy design feature. However, IRDAI requires:

- Clear disclosure in the policy schedule and Schedule of Benefits

- Proportionate deduction methodology must be clearly defined in policy wording (Clause 6 in standard policy wordings)

- Insurers must provide a standard definition of ICU in their policy wording and the ICU cap must be stated separately

IRDAI has issued warnings to insurers applying room-related deductions that were not clearly disclosed in the policy document. If you believe a deduction was applied to charges unrelated to room rent category, you can file a grievance with the insurer and escalate to IRDAI’s IGMS (Integrated Grievance Management System).

Plans With No Room Rent Sub-Limit (2026)

These plans as of 2026 carry no room rent cap (subject to the policy wording at the time of purchase — always verify):

| Plan | Insurer | Room Rent Policy |

|---|---|---|

| Optima Secure | HDFC Ergo | No room rent sub-limit |

| ReAssure 2.0 | Niva Bupa | Single private room, no cap |

| Supreme | Care Health | No room rent sub-limit |

| Comprehensive | Star Health | Single private room |

Plans with room rent sub-limits (check latest policy documents):

| Plan | Insurer | Room Rent Cap |

|---|---|---|

| Optima Restore | HDFC Ergo | Sub-limits on lower sum insured variants |

| Young Star | Star Health | 1% of SI per day on base plan |

| iCan | ICICI Lombard | Fixed cap on lower variants |

Important: Room rent policies can change when plans are updated. Always verify the current Schedule of Benefits at the time of purchase, not marketing summaries.

What to Do If Your Plan Has a Room Rent Cap

If you have an existing policy with a room rent sub-limit, there are steps to minimise exposure:

Before Planned Procedures

- Call the insurer’s TPA (or in-house claims team) before admission

- Ask them to confirm which room category is covered under your policy

- Request a pre-authorisation letter that specifies the permitted room category

- At the hospital, explicitly request a room at or below the permitted category

At Emergency Admission

- Accept whatever room is available initially

- Contact the insurer’s TPA within 24 hours of admission (required for cashless activation)

- Request a room transfer to a category within your sub-limit as soon as clinically feasible

- Document the room transfer request with the hospital and insurer in writing

At Policy Renewal

Consider porting to a plan with no room rent sub-limit. Under IRDAI’s portability guidelines, accumulated waiting period credits transfer when you port 45 days before renewal.

How to Check Your Policy’s Room Rent Clause

The room rent clause is in the Schedule of Benefits (also called Benefit Table or Summary of Cover) — a table in the first 3–5 pages of your policy document.

What to look for:

- “Room Rent” or “Room Category”: Fixed amount, percentage of SI, or “Single Private Room”

- “ICU/ICCU”: Separate cap, often 1.5–2× room rent limit, or “actual”

- “Room Upgrade”: Some policies allow room upgrades for specific conditions without proportionate deduction — check this clause

If your policy states “Single Private Room — No sub-limit”, proportionate deduction does not apply to room-related costs.