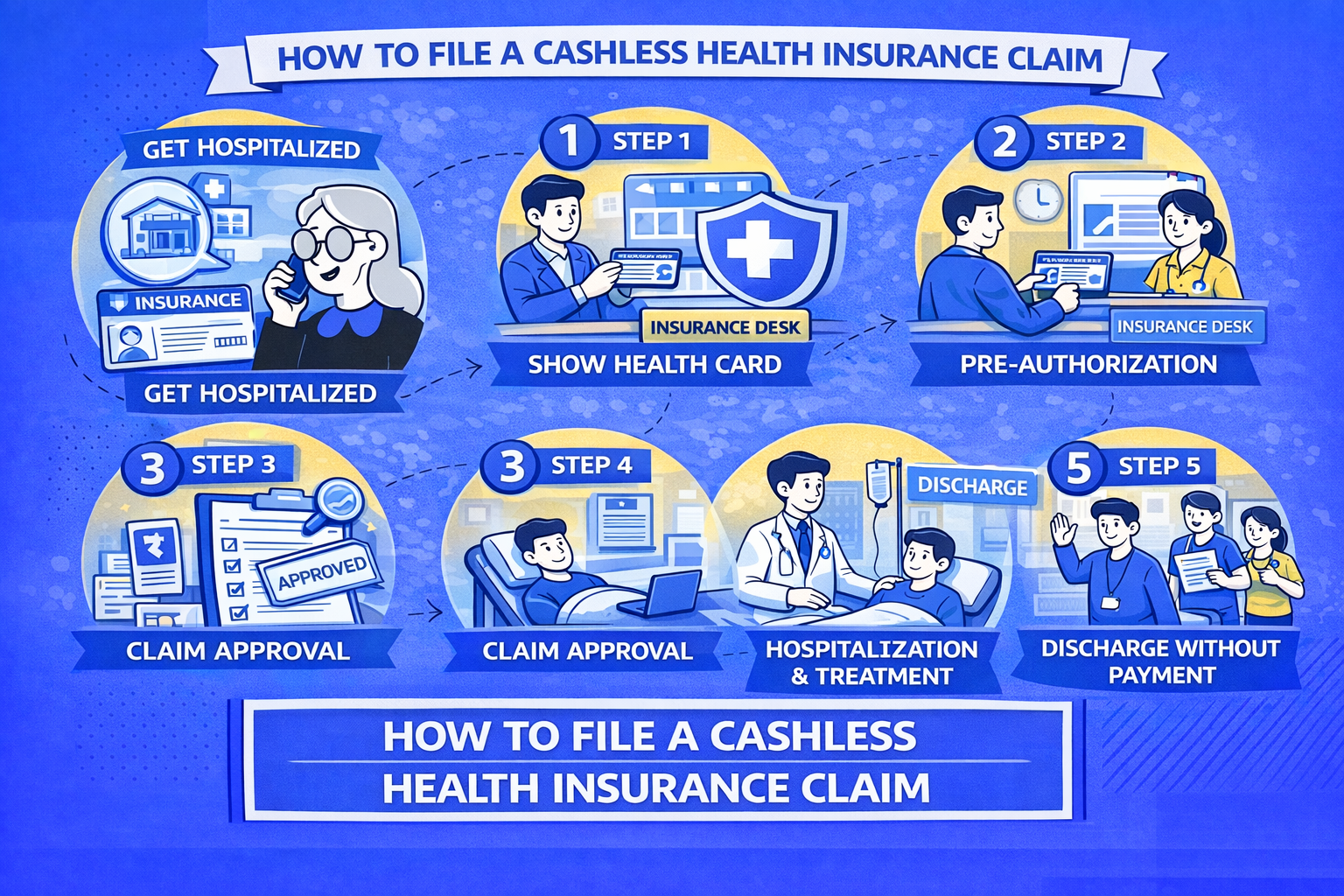

Cashless health insurance allows you to receive hospital treatment without paying out of pocket — the insurer settles the bill directly with the network hospital. The process involves a pre-authorisation step that both planned and emergency admissions require. Understanding each step prevents delays, partial approvals, and preventable out-of-pocket costs.

Before Hospitalisation: Preparation Steps

Verify Network Hospital Status

Before choosing a hospital for any planned procedure, verify it is in your insurer’s network. Go to the insurer’s website and search under “Network Hospitals” using the hospital name and city. Networks change — verify for each hospitalisation, not just once.

Keep Your Insurance Details Accessible

Have the following ready before reaching the hospital:

- Health insurance policy number

- Insurer name and cashless helpline number (print from the e-card)

- TPA name and helpline (if your insurer uses a TPA)

- E-health card or health card (available in most insurer apps)

For Planned (Elective) Procedures

Step 1: Inform the Insurer 3–5 Days in Advance

For planned surgeries, cancer treatment, or other elective procedures:

- Call the insurer’s cashless helpline 3–5 days before the procedure

- Provide: procedure name, hospital name, treating doctor’s name, estimated costs

- Request: pre-authorisation initiation number (confirm it is lodged in their system)

Why this matters: Pre-authorisation for planned procedures involves a medical review. Starting early ensures approval is obtained before the procedure date.

Step 2: Submit Pre-Authorisation at the Hospital

On admission day:

- Go to the hospital’s insurance desk or billing counter

- Present your e-health card and photo ID

- The hospital initiates a formal pre-authorisation request to the insurer/TPA (standardised NHCX form)

- The pre-auth includes: diagnosis, ICD-10 code, procedure, estimated cost, clinical notes

Step 3: Wait for Approval

- Insurer/TPA reviews the request (2–6 hours for standard procedures)

- Approval or query letter is sent to the hospital insurance desk

- If approved: you proceed with the procedure; the approved amount is locked

- If queried: hospital provides additional clinical information

Step 4: Procedure and Discharge

- Undergo the planned procedure

- At discharge, the hospital generates the final bill

- Hospital submits final bill to insurer; insurer processes settlement

- You pay: any co-pay, items not covered, room upgrades above policy limit, and the difference if the final bill exceeds the initial approval

For Emergency Admissions

Step 1: Admit and Seek Treatment Immediately

In an emergency, treatment comes first. Do not delay admission for insurance paperwork.

Step 2: Inform Insurer Within 24 Hours

Call the insurer’s cashless/claims helpline as soon as possible — ideally within 24 hours of admission. Most policies require this intimation period. Provide:

- Policy number and insured’s name

- Hospital name and treating doctor

- Diagnosis (if available)

- Estimated duration and procedure

Note: Some policies allow 48-hour intimation for emergencies. Check your specific policy’s emergency intimation window.

Step 3: Hospital Submits Pre-Authorisation

The hospital’s insurance desk submits the pre-auth request after emergency stabilisation. For emergency cases, a preliminary approval is typically issued quickly (30–60 minutes) to enable continued treatment.

Step 4: Ongoing Authorisation for Long Admissions

For ICU stays or extended admissions:

- The insurer may request clinical updates every 2–3 days

- Extension of authorisation is required for stays beyond initially approved duration

- The hospital’s insurance desk manages this process — stay informed of their interactions

Step 5: Discharge Settlement

At discharge:

- Hospital generates final itemised bill

- Submits to insurer for final settlement

- Insurer releases payment within 30–45 minutes of final document submission (for in-house teams)

- You receive a final settlement letter showing what was paid and any amounts you owe

What You Typically Pay at Discharge

Even with a cashless claim, out-of-pocket costs at discharge are common:

| Item | Why You Pay |

|---|---|

| Co-payment | Mandatory co-pay percentage in your policy |

| Room upgrade | If you chose a higher room category than your policy allows |

| Excluded items | Consumables (if not covered), cosmetics, OPD |

| Excess over approval | If final bill exceeds pre-authorised amount |

| Meals / Attendant charges | Generally excluded |

| Medicines bought outside | Pharmacy bills from outside the hospital |

When Cashless is Denied: Immediate Steps

- Do not leave the hospital — get the denial reason in writing from the insurance desk

- Call your insurer immediately — sometimes denials are processing errors corrected by a call

- Pay and claim reimbursement — if cashless is unavailable, pay the bills and file reimbursement within 15–30 days (per your policy’s reimbursement timeline)

- Keep all originals — discharge summary, all bills, prescriptions, investigation reports

- File grievance within 15 days — if the denial was incorrect, formal grievance escalation is the next step

Escalation Path for Cashless Disputes

- Level 1: Insurer’s Grievance Redressal Officer (GRO) — 15-day response window

- Level 2: IRDAI IGMS (igms.irda.gov.in) — submit complaint online

- Level 3: Insurance Ombudsman — free, binding resolution for claims up to ₹50 lakh (as per Insurance Ombudsman Rules, 2017, as amended in 2021)

Disclaimer: PolicyJack is an independent research platform. We do not sell insurance, receive commissions, or have commercial relationships with any insurer.