IRDAI’s Annual Report 2023-24 records that health insurers received over 2.6 crore claims in FY24. The claim rejection rate across the industry (claims refused as a percentage of claims received) remains a persistent consumer concern. Understanding why claims get rejected — and which reasons are avoidable — directly affects both the decision to buy a specific plan and how to manage a policy after purchase.

Reason 1: Non-Disclosure of Pre-Existing Conditions

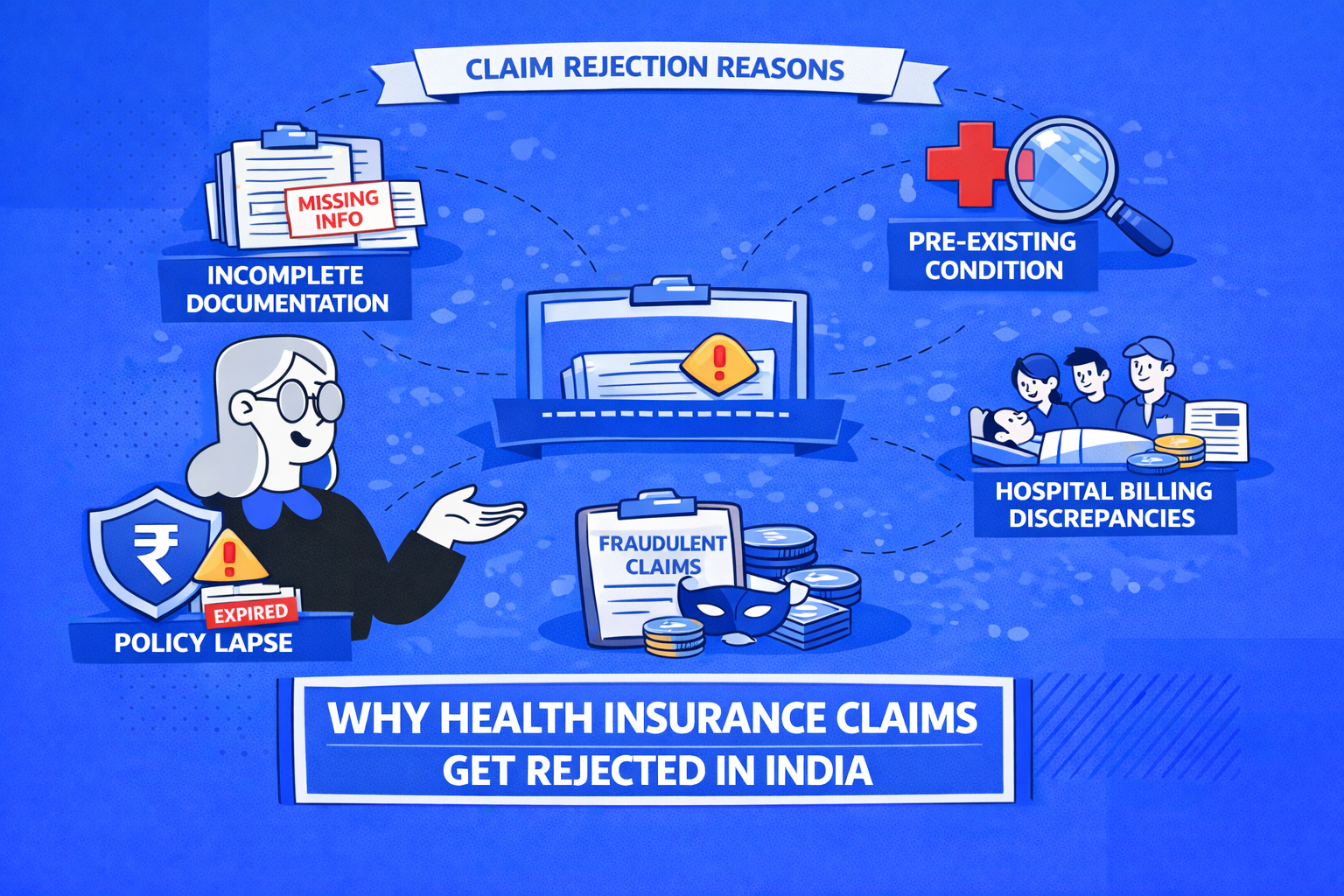

Non-disclosure is the most consequential and most avoidable cause of claim rejection. At the time of policy application, every health condition, treatment, or hospitalisation in the past must be declared accurately. Common non-disclosed conditions that lead to rejections:

- Hypertension (blood pressure medication that has been “normal” for years)

- Diabetes (even if well-controlled)

- Previous surgeries or hospitalisations

- Diagnostic tests showing abnormal results

- Psychiatric conditions or treatment history

- Alcohol or tobacco use history (relevant for liver or lung claims)

The cascading effect: Non-disclosure of one condition can void the entire policy, not just the claim related to that condition. IRDAI regulations limit insurers’ ability to contest claims after 8 years of continuous coverage without a break — but within those 8 years, any non-disclosure is contestable.

Action: Disclose everything, even conditions you believe are resolved or unrelated to the coverage you seek. The insurer will decide what loading or waiting period to apply — that is their role. Yours is disclosure.

Reason 2: Waiting Period — Treatment Filed Too Early

Every health insurance policy has multiple waiting periods:

| Waiting Period Type | Duration | What It Blocks |

|---|---|---|

| Initial exclusion period | 30–90 days from inception | All non-accident hospitalisations |

| PED (pre-existing disease) wait | 2–4 years (max 3 per IRDAI 2023) | Conditions existing before policy |

| Specific disease wait | 1–2 years | Named conditions (hernia, cataract, etc.) |

| Maternity wait | 2–4 years | Delivery and related expenses |

A claim filed during any applicable waiting period will be rejected as a contract violation. The 30-day initial exclusion means even a genuine illness in the first month is not covered.

Action: Map your specific waiting periods from the policy document to a calendar. Know exactly when each coverage type activates.

Reason 3: Policy Exclusions

Every policy has a list of conditions and treatments that are never covered, regardless of hospitalisation. Standard exclusions include:

- Dental treatment (unless due to accident)

- Vision correction (spectacles, contact lenses, LASIK in most plans)

- Cosmetic and aesthetic procedures

- Self-inflicted injuries

- Alcohol, drug, or substance-related treatments

- Infertility and assisted reproduction (unless add-on)

- War, terrorism, nuclear hazard

- Experimental treatments not approved by IRDAI/medical authorities

- Non-allopathic treatments (unless Ayush add-on is purchased)

Action: Read Section 10 (Exclusions) of your policy document before purchase, not after a rejection.

Reason 4: Insufficient or Incorrect Documentation

Claim processors require a specific set of documents to assess and approve claims. Missing or incorrect documentation is a common cause of rejection — not on merit, but on process.

Standard documents required for a reimbursement claim:

- Original hospital bills (itemised)

- Discharge summary with diagnosis and treatment details

- Doctor’s prescription and consultation notes

- Investigation reports (blood tests, imaging)

- Policy copy and ID proof

- Pharmacy bills with prescriptions

- Claim form (filled and signed by treating doctor)

Common documentation errors:

- Discharge summary missing ICD-10 diagnosis code

- Bills not itemised (lump-sum amounts are often queried)

- Pharmacy bills without corresponding prescription

- Claim form unsigned or incompletely filled

- Documents submitted after the claim submission deadline (typically 15–30 days post-discharge)

Action: Before discharge, ask the hospital for a complete discharge summary with all diagnosis codes. Keep originals of all bills. Submit within the time limit specified in your policy.

Reason 5: Policy Lapsed Due to Non-Payment

If a health insurance policy lapses (due to unpaid renewal premium) and hospitalisation occurs during the lapse period, no claim is payable. This is the simplest and most completely avoidable rejection reason.

IRDAI mandates a 30-day grace period after the renewal due date — if premium is paid within this window, the policy is renewed without a lapse. Claims during the grace period before premium payment may not be covered.

Action: Set premium payment reminders 30 days before renewal due date. Use auto-payment/standing instructions for renewal premium.

Reason 6: Daycare Procedure Not on the List

Hospitalisation for less than 24 hours is only covered if the specific procedure is on the plan’s daycare schedule. If the procedure was performed in less than 24 hours but is not on the daycare list, it must meet the standard 24-hour minimum — and if it doesn’t, it will be rejected.

Action: Before any planned short-duration procedure, verify with the insurer that it qualifies as a daycare procedure under your specific plan.

Reason 7: Treatment at Non-Network Hospital Without Approval

Some policies impose co-payment or partial coverage limitations for treatment at non-network hospitals. In rare cases, specific policy structures may reject entirely if a network hospital was available and reachable. More commonly, non-network hospital treatment is covered as reimbursement with a higher co-pay.

Action: For planned procedures, confirm network hospital availability first. For emergencies, inform the insurer within 24 hours.

Reason 8: Delayed Intimation

Most policies require you to inform the insurer (or TPA) of hospitalisation within specified time limits: typically 24–48 hours for emergency admission and 3–7 days for planned admissions. Delayed intimation can be used as grounds for rejection.

Action: Call your insurer’s helpline the moment you know about an admission — for emergencies, call as soon as a family member can. This call creates a timestamped record.

Reasons 9 & 10: Fraud and Experimental Treatments

Inflated bills, false diagnoses, and collusion between hospitals and policyholders are treated as fraud and result in both rejection and possible policy cancellation. Experimental or non-standard treatments not approved by medical authorities are excluded from coverage in most standard policies.

What to Do When a Claim Is Rejected

- Request written rejection notice with the specific policy clause cited

- Review the clause in your actual policy document — not just the rejection letter’s interpretation

- File a formal grievance to the insurer’s Grievance Redressal Officer (GRO) via registered post or the insurer’s online portal

- Escalate to IRDAI IGMS (igms.irda.gov.in) if unsatisfied after 15 days

- Approach Insurance Ombudsman for final binding resolution — free process, covers disputes up to ₹50 lakh (Insurance Ombudsman Rules, 2017 as amended in 2021)

Disclaimer: PolicyJack is an independent research platform. We do not sell insurance, receive commissions, or have commercial relationships with any insurer.